Alignment Healthcare ALHC has given investors a clearer profitability story, but the stock’s rally has made the buy case less straightforward.

The question now is not whether execution has improved. It has. The harder question is whether the current price still leaves enough room for upside after investors have already rewarded that progress.

ALHC Earnings Momentum Looks Real

First-quarter 2026 results showed that Alignment’s operating model is moving beyond a long-range profitability promise. Revenues rose 33.3% year over year to $1.23 billion, supported by membership expansion and higher per-member revenue.

The company reported earnings of 5 cents per share compared with a loss of 5 cents a year earlier. Adjusted EBITDA increased 87.6% to $37.9 million, while the Medical Benefit Ratio improved to 88.2% from 88.4%, signaling modestly better medical-cost control.

Membership reached about 284,800, up 30.9% year over year. Molina Healthcare MOH, another managed-care company with Medicare exposure, offers a useful comparison point for investors watching how government-sponsored health plans balance enrollment growth and medical costs.

Alignment Guidance Supports the Bull Case

Raised 2026 guidance supports the view that scale and margin expansion can continue together. Alignment expects full-year membership of 294,000-299,000 and revenues of roughly $5.160-$5.205 billion.

The adjusted EBITDA outlook of $138-$163 million points to continued operating leverage as the business grows. That matters because the bullish case depends on more than adding members. ALHC also needs automation, clinical management and plan quality to translate growth into better margins.

Surgery Partners SGRY, a healthcare-services company focused on surgical facilities and ancillary services, provides a broader sector reminder that execution models matter. For Alignment, the key model question is whether its clinical-first platform can keep higher-acuity growth profitable.

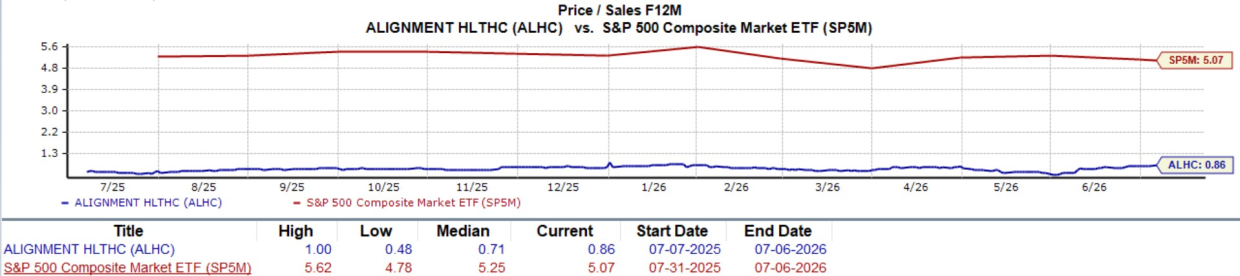

ALHC Valuation Sets a Higher Bar

The stock is not an obvious bargain after its advance. Shares were up 24.3% year to date and 79.1% over the trailing 12 months, well ahead of the Zacks Medical sector and the broader S&P 500 over those periods.

ALHC recently traded around 0.9X forward 12-month sales, above its five-year median of 0.7X. Better execution is being recognized, which means the next leg higher may require fresh estimate momentum, further margin proof or a more attractive entry point.

Image Source: Zacks Investment Research

ALHC’s valuation is still below broader market sales multiples, but that alone does not settle the debate. The company is being valued more richly than its own historical median, so investors need confidence that guidance can be met without utilization pressure eroding the earnings path.

Alignment Balance Sheet Adds Flexibility

Liquidity remains a meaningful support to the investment case. First-quarter operating cash flow climbed to $128.7 million from $16.6 million a year earlier, adding evidence that improved earnings are showing up in cash generation.

Alignment ended the quarter with about $726 million in cash, cash equivalents and short-term investments. Management expects 2026 capital expenditures near $40 million, mainly tied to software development and technology investments.

That flexibility gives Alignment room to fund technology, clinical infrastructure and measured expansion without stretching the balance sheet. It also helps absorb near-term variability tied to higher-acuity members, risk-model changes and revenue timing.

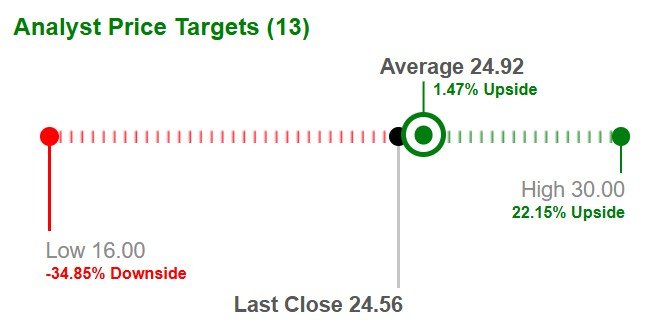

Based on short-term price targets offered by 13 analysts, the average price target of $24.92 represents an increase of 1.5% from the last closing price.

Image Source: Zacks Investment Research

What ALHC Ratings Say Now

The bottom line is balanced. ALHC has better profitability, higher guidance, stronger cash flow and a growing member base, but the stock already reflects a good portion of that operational progress.

The stock currently carries a Zacks Rank #3 (Hold), which is consistent with that setup. A Zacks Rank #3 can fit a stock with improving fundamentals but a less obvious near-term entry point after a sizable rally.

Alignment also has a VGM Score of B and a Growth Score of A, which support the long-term operating story. Its Value Score of C and Momentum Score of D are less favorable, suggesting investors may want more valuation support or renewed estimate momentum before treating ALHC as a more compelling buy.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

Alignment Healthcare, Inc. (ALHC) : Free Stock Analysis Report

Molina Healthcare, Inc (MOH) : Free Stock Analysis Report

Surgery Partners, Inc. (SGRY) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.