Arhaus, Inc. ARHS has become a more interesting retail name after recent share-price weakness, but the setup is not clean enough to call an aggressive entry point.

The stock offers a reasonable valuation and a debt-free balance sheet. Softer demand, tariff uncertainty and margin pressure still keep the near-term earnings case in wait-and-see territory.

ARHS Valuation Looks Reasonable on Paper

ARHS trades at 15.51X forward 12-month earnings, above the Zacks sub-industry multiple of 14.39X but below the broader sector multiple of 23X and the S&P 500 multiple of 21.05X. That places the stock in a middle ground rather than a clear bargain.

The $8.00 price target sits close to the recent $7.83 share price. That small gap suggests limited near-term upside unless the operating picture improves more clearly.

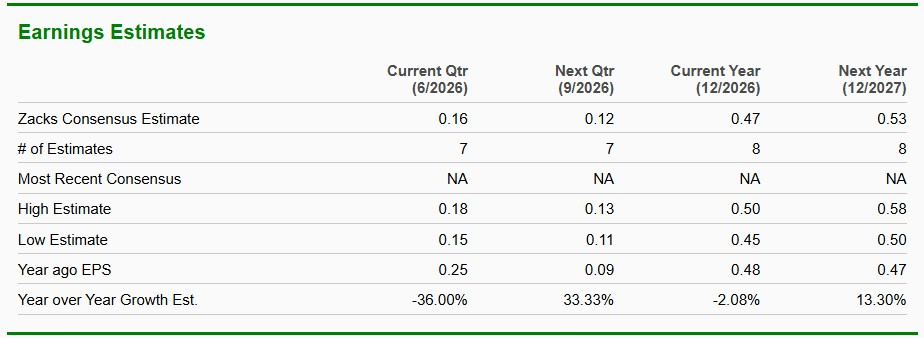

Image Source: Zacks Investment Research

Arhaus Balance Sheet Adds Downside Support

Arhaus ended the first quarter with $177.1 million in cash and cash equivalents and no long-term debt. That liquidity matters when discretionary home spending remains tied to a soft housing backdrop.

The balance sheet gives management room to fund showrooms, technology and infrastructure without adding financial strain. RH RH, a luxury home furnishings and lifestyle retailer, offers a useful peer reference for investors tracking demand among higher-income home customers.

ARHS Earnings Setup Still Needs Proof

First-quarter net revenue rose 0.9% year over year to $314 million and came in slightly above expectations. Earnings per share slipped to 2 cents from 3 cents in the prior-year period, while adjusted EBITDA declined 3.1% to $18 million.

Margins also need monitoring. Gross margin fell 70 basis points to 36.4%, pressured by fuel and occupancy costs, and adjusted EBITDA margin narrowed 30 basis points.

Image Source: Zacks Investment Research

Arhaus Has Catalysts but Also Clear Risks

The bull case rests on improving written sales trends, a 15% increase in client deposits to $271.2 million and a long runway for showroom expansion. Management still expects 10 to 14 showroom projects in 2026, including four to six new locations.

Technology investments are another potential support. Phase one of the Transportation Management System went live in April, with expected fiscal 2026 savings of $1 million to $2 million.

The bear case is still material. Comparable written sales fell 5.7% in the first quarter, and second-quarter comparable delivered sales are guided between down 5% and flat. Williams-Sonoma, Inc. WSM, an omnichannel home furnishings and lifestyle retailer, gives investors another benchmark for how home-related retail demand is holding up across the category.

Tariffs remain a key watch item, with 2026 impacts estimated at $30 million to $40 million. Net cash used in operating activities was $9.7 million in the first quarter, while investing outflows totaled $15.9 million.

ARHS Ratings Favor Patience Over Aggression

The bottom line is that ARHS has enough valuation and balance-sheet support to stay on investors’ radar, but the stock still needs firmer demand and earnings momentum before looking like a high-conviction retail entry.

The stock currently carries a Zacks Rank #3 (Hold), which points to a neutral near-term stance. Its Style Scores show a mixed profile, with a Value Score of B, Growth Score of F, Momentum Score of C and VGM Score of D. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

That split fits the broader setup. The Value Score supports the case that ARHS is not stretched, but the weak Growth Score and middling Momentum Score argue against chasing the stock. Patient investors may find the name worth watching, but the current evidence favors caution over urgency.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

Arhaus, Inc. (ARHS) : Free Stock Analysis Report

Williams-Sonoma, Inc. (WSM) : Free Stock Analysis Report

RH (RH) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.