Throughout history, the investment landscape has been a vibrant canvas, painted with a series of groundbreaking technological revolutions. Yet, none have truly matched the seismic impact that the internet had on corporate America. However, the arrival of the artificial intelligence (AI) era has captured the collective imagination of both seasoned professionals and everyday investors alike.

Estimates by PwC paint a vivid forecast of AI’s potential, with a projected $15.7 trillion boost to the global economy through enhanced productivity and consumption-side benefits by the close of this decade.

No entity has been more direct in reaping the rewards of the AI frenzy than Nvidia (NASDAQ: NVDA).

Image source: Getty Images.

Nvidia’s Remarkable Ascension Sets it Apart

The turn of the calendar to 2023 revealed Nvidia as a $360 billion colossus teetering on the brink of tech prominence. Fast forward to August 28, 2024, and the company stood at an awe-inspiring $3.09 trillion in market value. Briefly, in June, it claimed the throne as the most valuable publicly traded company following a landmark 10-for-1 stock split.

The meteoric rise of Nvidia, catapulting to over $3 trillion in less than a year and a half, can be ascribed to the unrivaled prowess of its H100 graphics processing unit (GPU), the premier choice for AI-accelerated data centers. This GPU functions as the brainpower behind generative AI solutions, the force driving the training of large language models (LLMs), and the lifeline of real-time decision-making by AI-powered software and systems.

The demand for Nvidia’s hardware has inundated supply, affording the company exceptional pricing leverage. While competitors like Advanced Micro Devices (NASDAQ: AMD) retail their MI300X AI-GPUs for $10,000 to $15,000, Nvidia’s H100 commands a heftier price tag ranging from $30,000 to $40,000.

CUDA, Nvidia’s software platform, has played a pivotal role in its success. As the backbone for developers constructing LLMs and maximizing the computing potential of their GPUs, CUDA has fostered unwavering customer loyalty towards Nvidia’s suite of products and services.

Unveiling six consecutive quarters of surpassing Wall Street’s sales and profit forecasts, Nvidia has been the epitome of a thriving enterprise.

However, despite these accolades, there lurks a subtle performance metric that portends a turning point for Nvidia.

First Sequential Decline in Two Years Spells Trouble

As observed earlier this week, it was hardly a shocker when Nvidia surpassed Wall Street’s revenue and earnings per share (EPS) estimates for the fiscal second quarter ending July 28. Analysts often err on the side of caution, setting a low bar for companies to sail over.

Yet, essential metrics such as revenue and net income only paint part of the picture.

In Nvidia’s case, the true barometer of its trajectory lies in its gross margin. While I personally prefer the adjusted gross margin, which excludes acquisition-related costs and stock-based compensation, either metric spells out the tale succinctly.

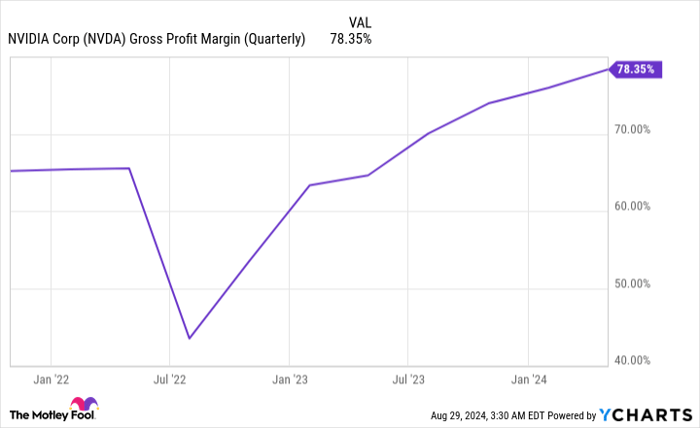

NVDA Gross Profit Margin (Quarterly) data by YCharts. Adjusted gross margin data through Nvidia’s fiscal first quarter.

During the fiscal first quarter ending April 28, Nvidia’s adjusted gross margin soared to a staggering 78.35%. Within five quarters, it surged by nearly 14 percentage points, a testament to the premium prices Nvidia commands for its AI-GPUs.

However, Nvidia had previously indicated an adjusted gross margin of 75.5% (+/- 50 basis points) for the fiscal second quarter in its first-quarter report. Achieving this range would mark the first sequential quarterly dip in adjusted gross margin witnessed in two years.

Post the bell toll on Wednesday, Aug. 28, Nvidia unveiled its highly-anticipated fiscal second-quarter results, showcasing a 320 basis point dip in adjusted gross margin to 75.15%. Though within the forecasted range from three months ago, it huddled towards the lower end of expectations.

Moreover, Nvidia’s guidance for the fiscal third quarter hints at potential further erosion in gross margin, spelling a tumultuous journey ahead.