Shopify Inc. SHOP entered 2026 with a payments ecosystem that is becoming more important to its monetization profile. While artificial intelligence remains a key part of the SHOP investment narrative, the company’s first-quarter 2026 results highlighted another meaningful growth lever: the rising share of gross merchandise volume (or GMV) processed through Shopify Payments and Shop Pay.

The increase in Shopify Payments penetration shows that the company is processing a larger share of the commerce activity already flowing through its platform. Shopify’s platform now extends well beyond storefront tools. The company is expanding its role in merchant operations by integrating payments, checkout, compliance, fraud detection, tax calculation, currency conversion and identity verification into its platform.

In the first quarter, Shopify Payments processed $67 billion of GMV, up 41% year over year. Payments penetration reached 67% of GMV, increasing three percentage points from the prior-year period. The steady rise indicates broader adoption of the company’s payment capabilities and gives SHOP more direct participation in merchant transaction volume.

The impact is already visible in Shopify’s revenue mix. Merchant Solutions revenues increased 39% year over year in the first quarter, driven primarily by GMV growth and higher Shopify Payments penetration. This outpaced Subscription Solutions’ revenue growth of 21%, highlighting the faster expansion of Shopify’s merchant services business during the quarter.

Shop Pay adds another layer to the opportunity. The checkout product processed $35 billion of GMV in the first quarter, up 59% year over year, while Shop Pay GMV outside the United States grew more than 70%. With Shopify Payments now available in 39 countries, deeper adoption across existing markets, Europe, Mexico and future new geographies remains an important watch point for SHOP’s payments-led revenue growth.

Shopify’s Competitor Landscape

Amazon.com, Inc. AMZN and Wix.com Ltd. WIX also operate commerce ecosystems, though their strategies differ from Shopify’s payments-led monetization focus. Amazon remains centered on its marketplace, Prime, fulfillment, advertising and third-party seller network. In the first quarter of 2026, North America revenues rose 12% year over year to $104.1 billion, while third-party sellers saw strong sales growth, particularly in the United States, Europe and Brazil.

Wix.com is closer to Shopify on the SMB and web-creation side, but its payments scale remains smaller. The company reported first-quarter 2026 GPV of $3.8 billion, up 12% year over year, while noting that GPV remained soft as SMBs faced macro pressure. WIX is also leaning into AI-powered online creation through Harmony and Base44.

Compared with Amazon’s marketplace-led model and WIX’s web-creation platform, SHOP remains more directly focused on merchant GMV monetization through Shopify Payments and Shop Pay. Shopify is not building a closed marketplace like Amazon or primarily a website-creation platform like Wix.com; instead, its execution depends on increasing payment penetration, strengthening checkout adoption and balancing transaction-linked growth with gross-margin dynamics.

SHOP’s Price Performance, Valuation & Estimates

Shares of Shopify have declined 18.9% in the past three months against the industry’s 24.1% growth.

SHOP’s Stock Three-Month Price Performance

Image Source: Zacks Investment Research

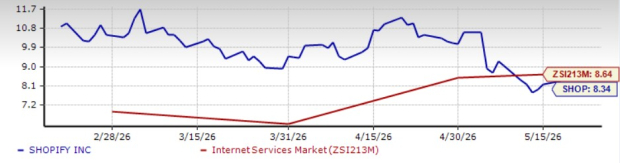

SHOP stock is currently trading at a discount. It is currently trading at a forward 12-month price-to-sales (P/S) multiple of 8.34, below the industry average of 8.64.

SHOP’s P/S Ratio (Forward 12-Month) vs. Industry

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for SHOP’s 2026 earnings implies a year-over-year increase of 53.9%. Estimates for 2026 earnings per share have increased in the past 30 days.

EPS Trend of SHOP Stock

Image Source: Zacks Investment Research

SHOP stock currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI’s Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren’t likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Wix.com Ltd. (WIX) : Free Stock Analysis Report

Shopify Inc. (SHOP) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.