The Illusion of Automatic Stock Market Gains

Interest rate cuts wield significant power over cash flow in money markets. Yet, the notion that such maneuvers inevitably spur stock market growth is a tale as old as time.

A recent revelation by JPMorgan strategists cautioned against assuming that the Federal Reserve’s anticipated rate reductions would directly translate into a fresh surge in stock values.

“The Fed may embark on easing measures, albeit reactively and in response to weakening growth—hardly adequate to propel the market to new highs,” they emphasized.

Investors often anticipate a flow of cash into equities as yields on money market instruments decline, anticipating a corresponding uptick in stock prices.

However, embedded in this “cash-on-the-sidelines” theory is a fundamental reality: each stock purchase involves an accompanying sale, making it a zero-sum game where no fresh capital truly pours into the market.

Stock trading symbolizes a continuous exchange where shares and funds shuttle between sellers and buyers.

Notably, in Initial Public Offerings (IPOs), the company and primary investors offload shares to new buyers, essentially transferring funds from one hand to another. Should secondary offerings take place, existing shareholders face dilution as their stakes diminish with the issuance of additional shares.

Yet, the fable of sidelined cash endures, especially amidst buoyant market sentiments. Renowned Portfolio Manager and CFA Charterholder Ben Carlson recently offered historical wisdom to debunk this myth.

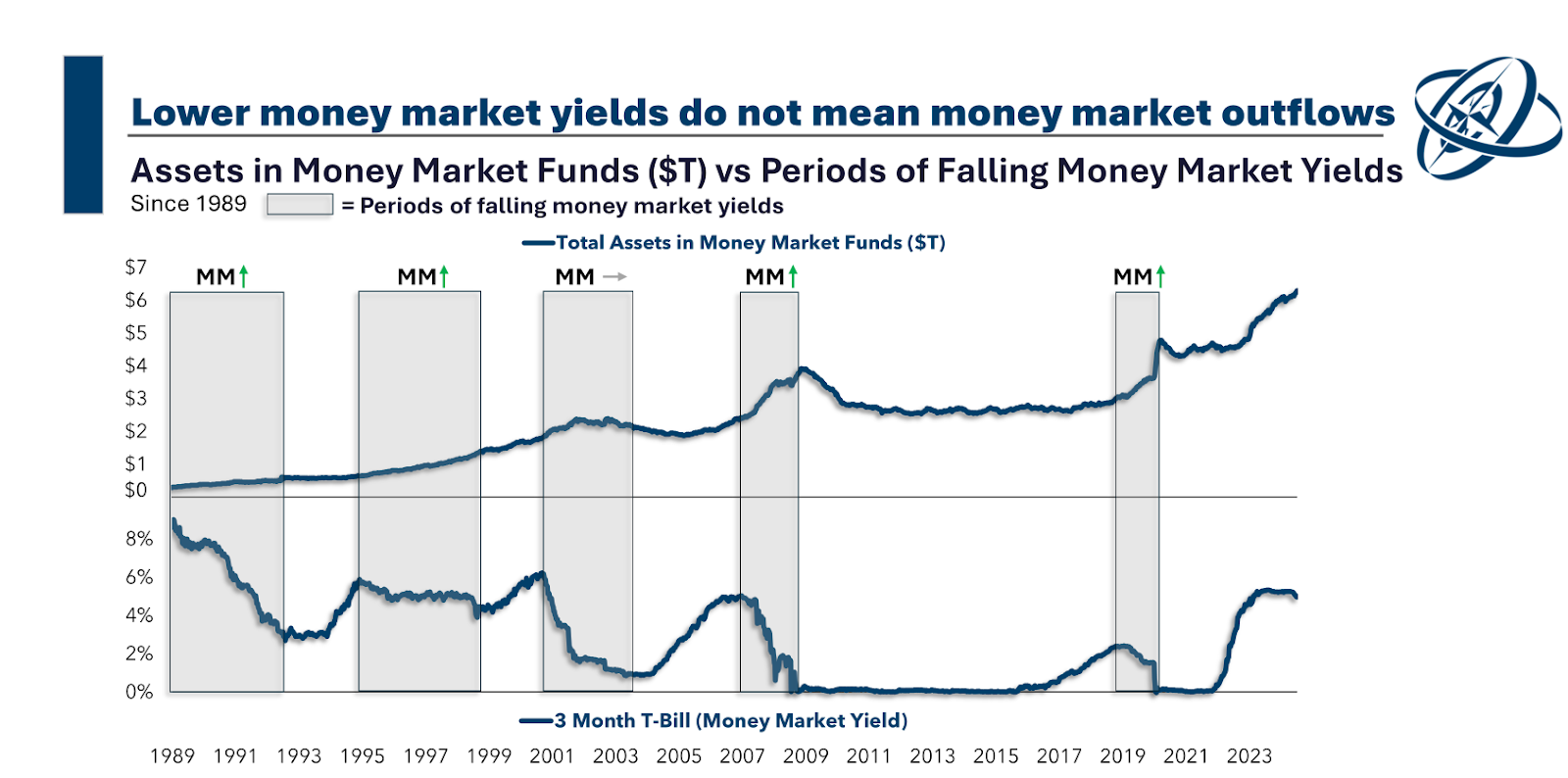

By scrutinizing past data, he illustrated that diminishing money market yields failed to trigger a significant outflow from these funds. Despite the current $6.3 trillion total in money market instruments, a figure double that of pre-pandemic levels, historical trends reveal that such yield declines have historically bolstered rather than dwindled these fund assets.

Notably, the cash in money market funds primarily serves purposes other than stock investments, such as emergency reserves, corporate funds, or allocations for short-term expenses. This money rests in liquid assets that guarantee safety and liquidity, emphasizing stability over growth. Despite interest rate declines, many investors opt to retain their funds in these instruments rather than face stock market volatility.

The interplay between interest rates and market dynamics harbors complexity. In times of plummeting yields, investors may pivot towards alternative safe havens like bonds instead of chasing stock market surges. Decreasing yields typically mirror a flight to security, with equities deemed too precarious to fit into this narrative.

However, the bond market faced tumult in recent years, marking a bleak period for fixed-income enthusiasts. Steep hikes in interest rates propelled the 10-year yield to nearly 5%—levels uncharted since July 2007.

Given the existing economic landscape characterized by historically elevated price-to-earnings (P/E) ratios, a protracted market consolidation appears feasible even in the event of a soft landing.

This scenario could usher in a phase where earnings growth plays a pivotal role in recalibrating market valuations, reducing inflated P/E ratios without necessitating fresh capital inflows. Thus, debunking popular myths, it is not cash influx but rather investors’ readiness to pay that dictates stock price oscillations.