Iridium Communications IRDM is set to unveil its third-quarter 2024 earnings prior to the market opening on Oct. 17.

Market analysts expect revenues to hit $205.7 million, reflecting an uptick of 4.1% compared to the previous year. The consensus on earnings per share remains at 20 cents, unmoved over the past 60 days. In the corresponding quarter last year, the company reported a loss of 1 cent.

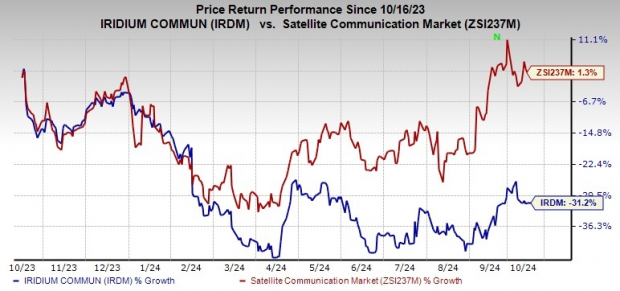

Over the last year, Iridium’s earnings surpassed the Zacks Consensus Estimate twice, fell short once, and met expectations once. The company experienced an average surprise of 202.2%. During this period, its shares plummeted by 31.2%, in stark contrast to the sub-industry’s 1.3% rise.

Image Source: Zacks Investment Research

Insights Leading to IRDM’s Q3 Earnings

Iridium’s Q3 performance is anticipated to thrive on surging revenue from the Service segment and an expanding subscriber base. Predictions foresee segmental revenues reaching $155.5 million, marking a 2.3% increase from the corresponding period last year.

One of the prime boosts is the strengthening commercial service revenues, driven notably by voice and data, IoT data, broadband, hosted payload, and other data service business lines. Projections point to commercial service revenues hitting $129 million, reflecting a 2.8% ascent from the previous year.

The uptrend in revenues from voice and data is attributed to the increased demand for Iridium’s push-to-talk services. Moreover, the commercial IoT segment is likely to benefit from consistent demand for personal satellite communications and conventional industrial services.

Furthermore, the Hosted payload and other data service segment is expected to gain from the new Iridium Satellite Time and Location offering.

Insight on Iridium Communications Inc Price and EPS Dynamics

Iridium Communications Inc price-eps-surprise | Iridium Communications Inc Quote

Growth in Engineering and Support revenues, particularly driven by increased engagement with the U.S. government, specifically ongoing projects related to the Space Development Agency contract, augurs well. IRDM anticipates a rise in revenues from the EMSS contract with the U.S. government in the latter half of 2024 following a “contractual step-up” in mid-September. Projections suggest quarterly revenues from the Engineering and Support segment to stand at $27.3 million, reflecting an 8.1% surge from the year prior.

There is an expectation of Subscriber Equipment revenues reverting to more standard levels as escalated demand, influenced by supply chain constraints and customer inventory buildup, normalizes. Projections for quarterly revenues from the Subscriber Equipment segment are at $21.2 million, indicating a 4% climb from a year ago.

Despite these positive shifts, macroeconomic frailty globally, alongside inflation concerns, emerges as a watchful challenge. Additionally, heightened competition within the satellite communications sector and escalating selling, general, and administrative costs, and research and development expenditures pose as potential headwinds.

Recent Significant Advancements

On September 25, 2024, Iridium secured approval from the 3rd Generation Partnership Project (3GPP) to broaden the capability of Narrowband Internet of Things (NB-IoT) for Non-Terrestrial Networks into the official Work Plan for 3GPP Release 19 (scheduled to wrap up in the fourth quarter of 2025). This milestone paves the way for global connectivity expansion through its latest service, Iridium NTN Direct, anticipated to stand as the world’s foremost global 5G NB-IoT service.

On September 19, 2024, Iridium unveiled its fourth stock repurchase authorization within four years. The $500 million authorization, greenlit by its board of directors, marks the largest in the company’s history. This extends the total buyback authorization to $1.5 billion through December 31, 2027.

Further, on September 3, 2024, the company introduced Iridium Certus GMDSS, marking substantial progress in maritime safety, compliance, and communication. These terminals constitute a pivotal element of any ship’s hybrid network system, offering enhanced cost structure, efficacy, and performance in maritime safety and security.

Forecasting IRDM Performance in Q3

Based on our reliable model, there is no definitive forecast for an earnings beat for Iridium this time around. The synergy of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) heightens the chances of an earnings beat. However, this scenario does not align in the current context.

Earnings ESP: Iridium possesses an Earnings ESP of 0.00%.

Zacks Rank: Iridium presently carries a Zacks Rank #2.

Stocks Worth Considering

Here are some notable stocks to mull over, given our model indicates their potential for an earnings beat this season:

Equifax EFX currently boasts an Earnings ESP of +1.56% accompanied by a Zacks Rank #2.

Equifax is due to unveil its third-quarter 2024 results on October 16. The Zacks Consensus Estimate for Equifax’s earnings and revenues for the upcoming quarter are set at $1.84 per share and $1.44 billion, respectively. EFX’s shares have advanced by 58.5% over the last year.

Netflix NFLX possesses an Earnings ESP of +1.37% alongside a Zacks Rank #2 at present. The company is slated to report its third-quarter 2024 results on October 17. The Zacks Consensus Estimate for the to-be-reported quarter for Netflix stands at $5.07 per share and $9.77 billion in revenues. Shares of NFLX have surged by 100.3% in the past year.

Abbott Laboratories exhibits an Earnings ESP of +0.18% paired with a Zacks Rank #2 presently. The company is set to announce its third-quarter 2024 results on October 16. The Zacks Consensus Estimate for Abbott projects earnings and revenues for the to-be-reported quarter at $1.20 per share and $10.56 billion, respectively. Shares of ABT have escalated by 25.9% in the past year.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.