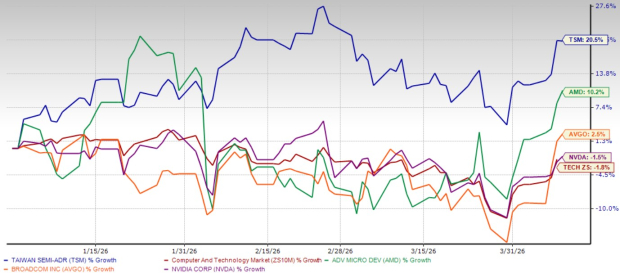

Taiwan Semiconductor Manufacturing Company TSM, also known as TSMC, has delivered an impressive 20.5% gain year to date (YTD), placing it among the best-performing technology stocks in the broader equity market amid ongoing macroeconomic challenges and geopolitical tensions. This performance easily beats the broader Zacks Computer and Technology sector, which has declined 1.8% YTD.

Taiwan Semiconductor is also among the top-performing semiconductor stocks, including Advanced Micro Devices, Inc. AMD, Broadcom, Inc. AVGO and NVIDIA Corporation NVDA. YTD, shares of Advanced Micro Devices and Broadcom have risen 10.2% and 2.5%, respectively, while NVIDIA has declined 1.5%.

This outperformance shows investors are becoming increasingly confident in Taiwan Semiconductor’s long-term story, even in a volatile market shaped by trade conflicts and geopolitical risks. We believe this momentum is grounded in strong fundamentals, and TSMC’s long-term outlook justifies a hold position for now.

Taiwan Semiconductor YTD Price Return Performance

Image Source: Zacks Investment Research

AI Boom Aids TSMC’s Prospects

Taiwan Semiconductor continues to lead the global chip foundry market. Its scale and technology make it the first choice for companies driving the AI boom. NVIDIA, Advanced Micro Devices and Broadcom all count on TSMC to build advanced graphics processing units (GPUs) and AI accelerators.

AI-related chip sales have become a major driver. In 2025, high-performance computing (HPC), which includes AI-related revenues, accounted for 58% of total revenues, up from 51% in 2024. Taiwan Semiconductor’s long-term forecasts depict that the momentum is far from over. Management expects AI revenues to increase at a CAGR of more than 50% over the five years from 2024 to 2029, which makes TSMC central to the AI supply chain.

To keep up with the growing demand for AI chips, Taiwan Semiconductor is spending aggressively. The company is set to invest between $52 billion and $56 billion in capital expenditures in 2026, far outpacing its $40.9 billion investment in 2025. The bulk of this spending is focused on advanced manufacturing processes, ensuring TSMC remains ahead of rivals in the chip manufacturing space.

TSMC’s Resilient Financial Performance

Taiwan Semiconductor has been benefiting from the AI boom by manufacturing advanced chips for major AI clients like Advanced Micro Devices, NVIDIA and Broadcom, which has led to record profits and a significant increase in revenues.

In the latest concluded financial cycle for 2025, TSMC’s revenues jumped 35.9% year over year to $122.42 billion, while earnings per share soared 51.3% to $10.65. This growth was powered by the booming demand for its advanced 3nm and 5nm nodes, which now account for more than 60% of total wafer sales. Gross margins improved 380 basis points to 59.9%, reflecting better cost efficiencies.

Taiwan Semiconductor Manufacturing Company Ltd. Price, Consensus and EPS Surprise

Taiwan Semiconductor Manufacturing Company Ltd. price-consensus-eps-surprise-chart | Taiwan Semiconductor Manufacturing Company Ltd. Quote

Buoyed by strong demand for its 3nm and 5nm chips, Taiwan Semiconductor anticipates continued revenue growth momentum in 2026. The company now forecasts 2026 revenues to increase approximately 30%. The Zacks Consensus Estimate for full-year 2026 revenues is pegged at $160.67 billion, indicating year-over-year growth of 31.2%.

Near-Term Risks Persist for TSMC

Despite its strengths, Taiwan Semiconductor witnesses near-term hurdles. Softness in key markets like PCs and smartphones may dampen its near-term prospects. According to a report by the International Data Corporation, these traditionally strong revenue drivers are projected to see a decline in shipments in 2026, limiting Taiwan Semiconductor’s growth despite rising AI demand.

The company’s global expansion strategy adds further strain. New fabs in the United States, Japan and Germany are vital for geopolitical risk mitigation, but they come with higher costs. Taiwan Semiconductor is estimating a near-term margin dilution of around 2%, which could further expand to 3-4% as production scales, due to higher labor and energy costs, along with lower utilization rates in the early stages.

Escalating geopolitical tensions, particularly U.S.-China relations, pose strategic risks. With significant revenue exposure to China, Taiwan Semiconductor is vulnerable to export restrictions, supply-chain disruptions or further regulatory pressure. These uncertainties could weigh on near-term performance.

An ongoing war between the United States and Iran creates immediate risks for Taiwan Semiconductor. The primary near-term threats involve energy supply disruptions in Taiwan, critical material shortages and increased volatility in chip production costs. The conflict has prompted concerns about the closure of the Strait of Hormuz, a vital shipping lane. As Taiwan imports nearly 95% of its energy needs and relies heavily on liquefied natural gas, a disruption to this route directly threatens the stability of Taiwan’s electrical grid, which is essential to keeping TSMC’s 24/7 fabrication plants running.

Semiconductor fabrication requires specialty gases like helium. Qatar, a key supplier of helium, has seen its Ras Laffan facility go offline due to Iranian drone strikes, cutting a significant portion of the global supply. While Taiwan Semiconductor likely has inventory buffers, a prolonged shortage could slow production schedules. The war is also threatening supplies of other crucial materials, including sulfur and bromine, used in semiconductor processing.

TSMC’s Premium Valuation Warrants a Cautious Approach

Taiwan Semiconductor stock isn’t cheap, as reflected by its Zacks Value Score of D. Looking at the current valuation multiple, it trades at a forward 12-month price-to-earnings (P/E) of 23.94X compared with the sector average of 23.46X.

Taiwan Semiconductor Forward 12-Month P/E Ratio

Image Source: Zacks Investment Research

Compared with other major semiconductor players, Taiwan Semiconductor has a lower P/E ratio than Broadcom and Marvell Technology, but has a higher ratio than NVIDIA. Currently, Broadcom, NVIDIA and Marvell Technology trade at P/E multiples of 25.84, 21.84 and 29.26, respectively.

Conclusion: Hold TSM Stock for Now

Taiwan Semiconductor remains a cornerstone of the semiconductor industry. Its unmatched capabilities in advanced chip manufacturing, strong exposure to AI demand and expanding capacity give it a solid long-term trajectory.

However, premium valuation and short-term headwinds, including weakness across the consumer end market, global expansion pressures and geopolitical friction, call for a more cautious stance.

Currently, Taiwan Semiconductor carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don’t build. It’s uniquely positioned to take advantage of the next growth stage of this market. And it’s just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it’s positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>

Advanced Micro Devices, Inc. (AMD) : Free Stock Analysis Report

NVIDIA Corporation (NVDA) : Free Stock Analysis Report

Broadcom Inc. (AVGO) : Free Stock Analysis Report

Taiwan Semiconductor Manufacturing Company Ltd. (TSM) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.