Established companies that have a whopping 50 years of dividend history under their belt are known as Dividend Kings, a testament to their remarkable consistency in both performance and earnings growth. Many of these Kings are traditional industry leaders found in more stable sectors such as consumer staples, utilities, or healthcare. However, one particular standout among them is Illinois Tool Works (NYSE: ITW), commonly referred to as ITW.

A Competitive Edge

The industrial conglomerate ITW features diverse business segments across varied industries such as automotive, food equipment, test and measurement, electronics, welding, polymers and fluids, construction products, and specialty products. Unlike other conglomerates like Honeywell or 3M that have underperformed the market, ITW has outshone the market over the last five years. With a noteworthy total return of 119.4% (including dividends) compared to the S&P 500’s 100.6%, ITW’s stock experienced an 18.9% surge last year, a commendable performance despite coming in lower than the S&P 500’s 24.2% increase.

ITW’s ability to keep pace with the market’s gains is particularly impressive given the dominance of megacap tech stocks. The company’s success lies in its commitment to growth and a viable strategy that could make investing in its stock a worthwhile prospect, even as it hovers around its all-time high.

Image source: Getty Images.

Riding on Quality Growth

Investing in a stock is essentially a bet on future earnings surpassing present figures. Companies that are yet to turn profit but are expected to deliver substantial growth in the future command high investor interest. Conversely, profitable yet slow-growing companies like ITW do not command hefty premiums due to the anticipation of modest future earnings. Though ITW’s price-to-earnings ratio of 24.6 is not exorbitant in relation to the market, it is still far from being cheap. This situation obligates the company to demonstrate quality and reliability to justify its valuation.

For a diversified industrial conglomerate like ITW, boosting earnings is primarily achieved through three avenues – acquisitions, increased sales volume, and enhanced margins. While ITW hasn’t extensively pursued acquisitions, it has opted to streamline its business to drive sales and margins.

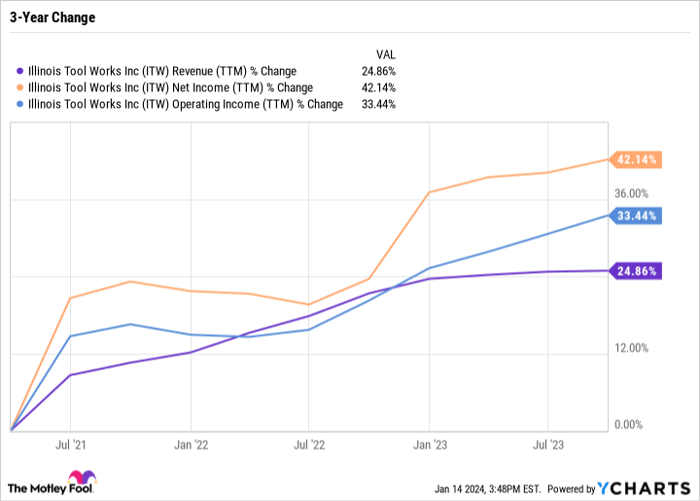

In the chart below, observe the faster growth in ITW’s net income relative to its revenue, usually an indicator of margin expansion:

ITW Revenue (TTM) data by YCharts

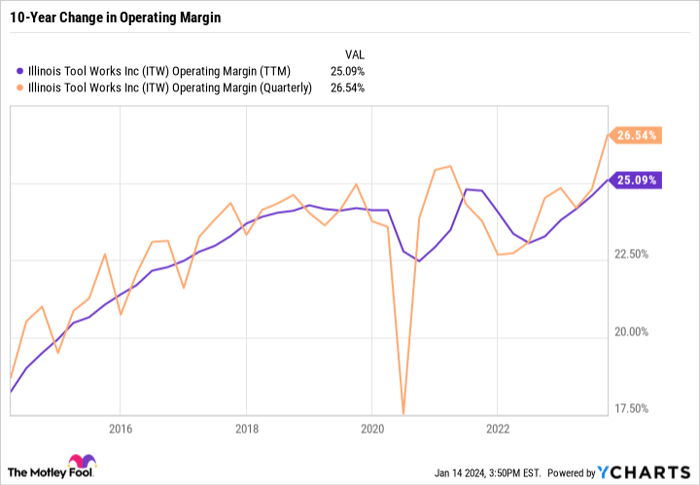

Here is another chart showcasing the upward trajectory of ITW’s operating margin:

ITW Operating Margin (TTM) data by YCharts

During the third quarter, ITW achieved its highest-ever quarterly operating margin of 26.5%, propelling the trailing-12-month operating margin to above 25%, a record high. This puts ITW in the league of the most efficiently run and powerful companies globally. For context, Apple holds an operating margin of 29.8%.

Sharp Focus on Margins

ITW’s primary emphasis lies on efficiency rather than sales growth. The company aims to achieve a 30% operating margin by 2030, coupled with an annual earnings-per-share growth of 9-10%, a 7% annual dividend increase, and a 4% average annual organic growth. With moderate organic growth and margin expansion, ITW is well-positioned for substantial earnings growth, supporting both dividend growth and buybacks.

In terms of buybacks, ITW has reduced its outstanding share count by 27.1% over the last decade. Apple, renowned for its aggressive stock buybacks, has witnessed a 35.5% reduction in its share count over the same period. Despite this, ITW has outpaced Apple in dividend growth, showcasing strong margins and buybacks that place it in the same league as the tech giant.

One of the keys to ITW’s success has been its approach to treating each business segment as an independent entity, empowering them to take risks while leveraging the company’s overall strength. During its 2023 investor day presentation, ITW provided a breakdown of its operating margins by segment compared to its competitors, unveiling higher margins in every single category.

Auto OEM | Food Equipment | Test and Measuring and Electronics | Welding | Polymers and Fluids | Construction Products | Specialty Products | |

|---|---|---|---|---|---|---|---|

ITW | 17% | 25% | 26% | 31% | 27% | 26% |