Apparel giants like Lululemon LULU and Nike NKE are not immune to concerns about a slowdown in consumer spending with both stocks down roughly -8% over the last year. However, Lululemon continued to reaffirm its attractive growth prospects are still intact after beating Q1 top and bottom-line expectations on Wednesday with Nike set to report its quarterly results later in the month.

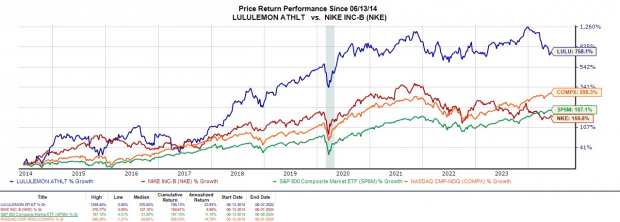

Seeing that LULU has dropped -37% year to date, investors may be wondering if it’s time to buy stock in the popular yoga-themed athletic apparel company for a rebound considering its blazing historical performance.

Image Source: Zacks Investment Research

Q1 Review & Revenue Outlook

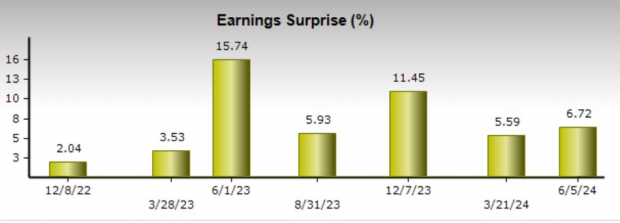

Illustrating that its brand loyalty remains strong, Lululemon’s Q1 sales of $2.2 billion rose 10% from the comparative quarter and slightly edged estimates of $2.19 billion. Furthermore, Q1 EPS of $2.54 came in 7% better than expected and spiked 11% from a year ago. It’s also noteworthy that Lululemon has now surpassed earnings expectations for 16 consecutive quarters dating back to September of 2020.

Image Source: Zacks Investment Research

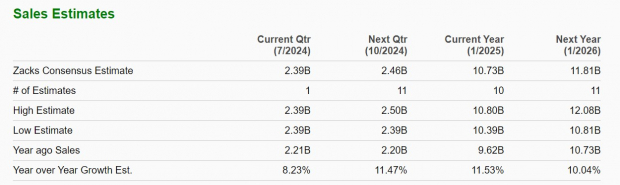

For the second quarter, Lululemon expects 9%-10% revenue growth which came in slightly above the current Zacks Consensus of 8.23% growth or sales of $2.39 billion (Current Qtr below). The company still expects full-year revenue growth in the range of 10%-11% with expectations calling for 11.53% growth (Current Year).

Image Source: Zacks Investment Research

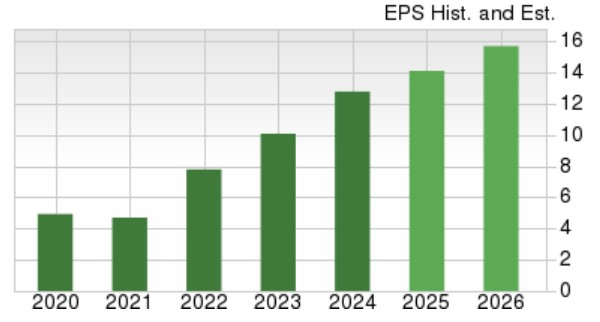

Based on Zacks estimates, Lululemon’s annual earnings are expected to rise 11% in its current fiscal 2025 to $14.14 per share versus EPS of $12.77 in FY24. Better still, FY26 EPS is forecasted to jump another 11% to $15.68.

Image Source: Zacks Investment Research

Key Takeaways

Despite lingering concerns of slower consumer spending, especially among premium apparel items, Lululemon’s stock lands a Zacks Rank #3 (Hold). To that point, Lululemon’s Q1 results helped reconfirm what is still an attractive earnings outlook.

Plus, LULU trades near its cheapest P/E valuation since going public at 22.9X and longer-term investors could be rewarded from current levels although there may still be better buying opportunities ahead.

Zacks Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.