When it comes to rivalries, few can match the history and fierceness between Ford Motor Company (NYSE: F) and General Motors (NYSE: GM). You could compare it to some of the greatest rivalries in sports, such as the Yankees vs. Red Sox, the Lakers vs. Celtics, or even other business rivalries, such as Coca-Cola vs. PepsiCo.

While Ford and GM are fierce rivals, they often make many similar strategic moves. However, in this case, it’s about time Ford does something its crosstown rival has been doing: share buybacks.

General Motors wasn’t shy about its strategy to return value to shareholders through share buybacks. It’s a simple strategy where the company purchases its own shares from the market and cancels them to reduce the number of shares in circulation, thereby increasing the value of the remaining shares. For shareholders, this means higher earnings per share and a higher return on future dividends.

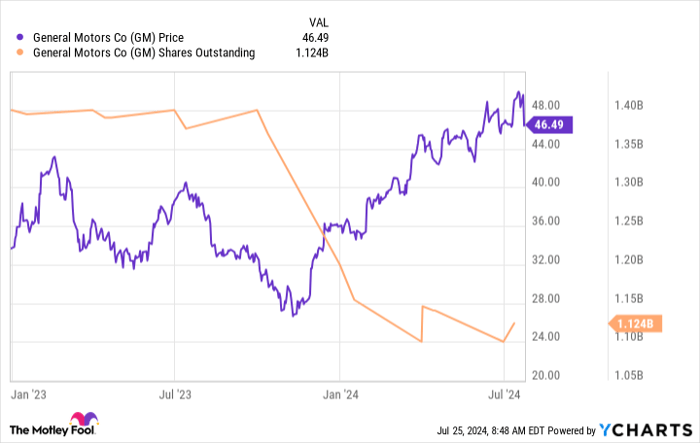

GM announced a large $10 billion buyback on Nov. 29, and then later announced a new $6 billion share repurchase authorization with a target of reducing its shares outstanding to less than one billion. The automaker ended the second quarter with a roughly 1.14 billion fully diluted share count, which was down 18% year over year, and you can see the progress made over time in the graph below.

Ford’s Course of Action

Ford could easily follow its crosstown rival’s lead and announce a large share buyback. After all, Ford has a strong balance sheet with roughly $27 billion in cash and roughly $45 billion in liquidity. During the second quarter, it increased its healthy free cash flow guidance to a range of $7.5 billion to $8.5 billion, and it’s long targeted returning 40% to 50% of adjusted free cash flow to shareholders.

So, what’s holding Ford back, you might ask? Well, here’s where things get a little murky. The Ford family still owns about 40% of the voting power in Ford company shares, and it’s well known that the family loves their dividends. According to Barrons, Ford could generate $21 billion in free cash flow over the next three years, and paying out 50% of that would equate to roughly $2.60 per share. That would be in addition to the quarterly $0.15 per share dividend and on top of any supplemental dividends the company often dishes out.

Another possible reason Ford is hesitant is because of its valuation, which sits at a price-to-earnings ratio of about 11.6 compared to General Motors’ multiple of 5.2, suggesting GM’s shares are more enticing to buy back than Ford’s, currently. However, that doesn’t excuse Ford from not having bought back shares in 2022 when the stock largely traded below 8 times earnings throughout the year.

The Controversial Stand

The Ford family will always opt for dividends over share buybacks, and Ford noted on its second-quarter conference call that the automaker believes it has better opportunities for its cash than buybacks. Further, as the Ford family owns a different class of shares that wouldn’t be involved in a share repurchase program, the future value of their dividends wouldn’t increase as common shares would, and every dollar spent on buying back common shares is a dollar not flowing to the family dividend.

However, with such a strong balance sheet, these things shouldn’t be mutually exclusive. It’s reasonable to think Ford could authorize a $5 billion share buyback program while still dishing out its quarterly and supplemental dividends to a healthy and valuable degree.

Ford’s near-term looks to be bumpy as the company tries to improve its production efficiency and lessen complexity, loses billions on its Model e division, and tries to fix quality issues that are sharply increasing warranty costs — it could use a positive catalyst.

It might be unpopular with the Ford family, but with the automaker’s stock down 23% over the past decade, Ford should double down on returning value to shareholders by initiating a share repurchase program if the stock’s price-to-earnings ratio again dips below 10 times earnings.

Considering Investment in Ford Motor Company

Before you buy stock in Ford Motor Company, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Ford Motor Company wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $692,784!*.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 29, 2024