Micron Technology, Inc. MU is benefiting from one of the strongest pricing environments the memory industry has seen in years. Higher DRAM and NAND prices, fueled by artificial intelligence (AI)-driven demand and limited supply, are pushing the company’s margins to multi-year highs.

In the second quarter of fiscal 2026, Micron Technology reported revenues of $23.86 billion, up 196% year over year and 75% sequentially. The company’s non-GAAP gross margin also improved sharply as stronger pricing and a richer product mix boosted profitability. The fiscal second-quarter non-GAAP gross margin reached an all-time high of 74.9%, improving from the year-ago quarter’s 37.9% and the previous quarter’s 56.8%. Demand for high-bandwidth memory (HBM), server DRAM and enterprise SSDs played a major role in this improvement.

AI servers are becoming a major growth engine for the memory market. These systems require far more memory capacity and bandwidth than traditional servers, increasing DRAM and NAND content per machine. As hyperscalers continue investing heavily in AI infrastructure, Micron Technology is benefiting from strong pricing power across its memory portfolio.

Supply conditions are also helping. Industry capacity remains tight, and new fabs will take years to ramp up meaningfully. This supply-demand imbalance is supporting higher average selling prices, which directly improves Micron Technology’s margins because memory manufacturing carries high fixed costs.

Overall, strong memory pricing and AI-led demand trends suggest MU’s margin momentum may continue in the near future. For the third quarter of fiscal 2026, Micron Technology projects a non-GAAP gross margin of approximately 81%, indicating a robust expansion from the year-ago quarter’s level of 39%.

Micron Peers Also Benefit From Strong Margin Trends

NVIDIA Corporation NVDA and Advanced Micro Devices, Inc. AMD are two major U.S.-listed semiconductor companies also benefiting from the AI boom, though their business models differ from Micron Technology.

NVIDIA continues to lead the AI accelerator market, with data center revenues growing 92% year over year in the recently reported first-quarter fiscal 2027 results. The company’s non-GAAP gross margin reached 75% from 60.8% in the year-ago quarter, supported by strong pricing power for its AI GPUs and networking products. NVIDIA’s growth indirectly benefits Micron Technology because AI servers using NVIDIA chips require large amounts of DRAM and HBM memory.

Advanced Micro Devices is also gaining momentum in AI and data center markets. Its EPYC server processors and Instinct AI accelerators are helping expand enterprise adoption. AMD’s data center revenues surged 57% year over year to a record $5.78 billion in the first quarter of 2026, while non-GAAP gross margins expanded 180 basis points to 55.4%. As AI server deployments rise, Advanced Micro Devices’ growth is increasing demand for advanced memory and storage products supplied by Micron Technology.

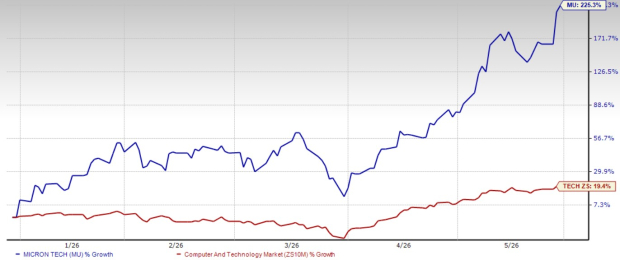

Micron’s Price Performance, Valuation and Estimates

Shares of Micron Technology have surged around 225.3% year to date compared with the Zacks Computer and Technology sector’s return of 19.4%.

Micron Technology YTD Price Return Performance

Image Source: Zacks Investment Research

From a valuation standpoint, MU trades at a forward price-to-earnings ratio of 10.37, significantly lower than the sector’s average of 26.02.

Micron Technology 12-Month Forward P/E Ratio

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Micron Technology’s fiscal 2026 and 2027 earnings implies a year-over-year increase of 611% and 70.2%, respectively. Bottom-line estimates for fiscal 2026 and 2027 have been revised upward in the past 30 days.

Image Source: Zacks Investment Research

Micron Technology currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA’s enormous potential back in 2016. Now, he has keyed in on what could be “the next big thing” in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

Advanced Micro Devices, Inc. (AMD) : Free Stock Analysis Report

Micron Technology, Inc. (MU) : Free Stock Analysis Report

NVIDIA Corporation (NVDA) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.